Workforce and Payroll

With some exceptions, staff levels have remained consistent throughout the pandemic.

Over half (52%) of providers were extremely or moderately concerned that staff layoffs or furloughs would be necessary at the beginning of the pandemic. Thankfully, most organizations were able to avoid such measures: 71% reported an increase or no change in staff levels as of early 2021, 12% reported a little, and 18% reported some.

FIGURE NUMBER 4.6

Level of concern about staff layoffs or furloughs

These results confirm what we heard in our interviews from May 2020. At that time, a fair number of organizations mentioned that some staff had their hours reduced, but these were nearly all temporary measures. Only four providers reported minor or large-scale reductions in staff levels. Of those four, two reported reductions of five or more staff, and two reported reductions of less than five staff. (Thirteen reported no change.)

Providers that were forced into temporary or permanent layoffs were generally smaller than average, or had significant numbers of employees in retail operations. The ReStore operations for both Habitat for Humanity affiliates were particularly affected; however, most of those workers were eventually retained via payroll assistance and the phased reopenings of retail businesses later in 2020.

FIGURE NUMBER 4.7

Changes to staff levels and activities

Some providers have actually expanded their staff capacity during the pandemic. In fact, four reported increases in total staff between March and May of 2020. Many of these new positions are supported by increased public grants and private giving levels over the past year; as such, those hires generally help administer programs that were created or expanded during the pandemic. However, some providers expressed concerns that scaled back funding in the future would result in the elimination of these new employees.

Today, four in five providers (82%) are only slightly or not at all concerned about future layoffs. Just two organizations expressed extreme or moderate concern. Those worries are likely due to continued anxiety over long-term revenue opportunities, and are possibly specific to new hires brought on during the pandemic.

Staff remained flexible to meet new challenges.

Almost three in four organizations (71%) responded that they had repurposed staff in some way since March 2020: 47% reported a little, and 24% reported some or a lot. In certain cases, these were reshuffled duties in the wake of temporary layoffs or furloughs for fellow workers. In other cases, staff were tasked with additional responsibilities as the result of new protocols, preograms, and client needs brought on by COVID-19.

Overall, many staff have been forced to demonstrate resilience and creativity throughout the pandemic; these efforts were widely lauded by leaders we interviewed. However, these changes also resulted in increased levels of stress and fatigue. One possible solution that over half (56%) of respondents said was very important or important: hazard pay and other financial benefits.

The Payroll Protection Program prevented a major disaster.

Introduced in the CARES Act, the PPP was a remarkable lifeline for thousands of businesses and nonprofits across the country. Housing providers in Richmond were no exception. During our first round of interviews in 2020, we learned that every organization that applied for a PPP loan received one.

According to leaders we interviewed, PPP loans were important in two ways:

- First, by allowing organizations to maintain payroll, rehire laid off or furloughed employees, and avoid downsizing. They were particularly helpful lifelines for both Habitat affiliates operating ReStore retail operations.

- Second, by ensuring that core operations were not affected, maintaining continuity of programs, and guaranteeing quality care to clients. In many cases, PPP also allowed other resources to be leveraged and deployed for other measures.

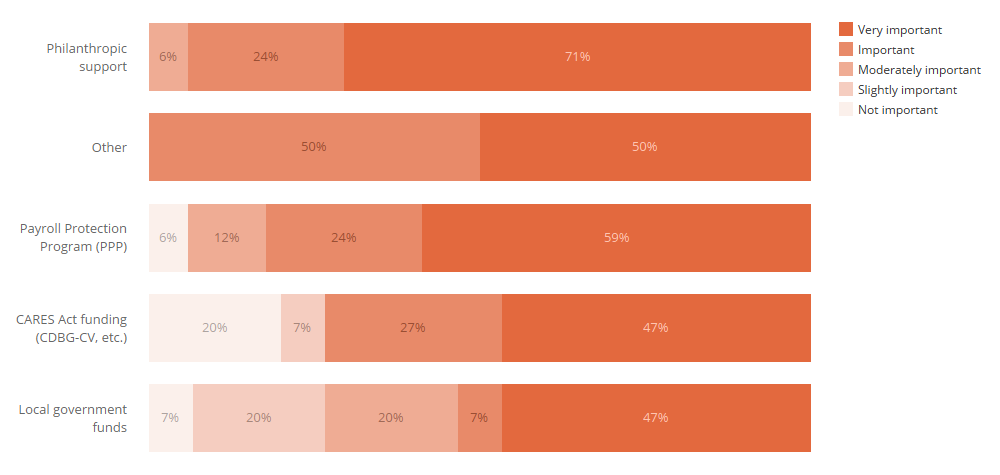

FIGURE NUMBER 4.8

Importance of financial relief sources

Over four in five (83%) providers rated PPP as important or very important to the solvency of their organization. Unfortunately, across the country, not every business that applied for PPP was successful in receiving assistance. We attribute the 100% success rate among Richmond’s housing nonprofits to the long-standing relationships many have with local and regional community banks in the region.

Only a couple of organizations admitted they did not apply for PPP. These providers made early, intentional decisions to forego the option based on their current operations and financial status, after consultation with executive leadership and advisors.

While December’s federal relief bill allowed certain businesses to apply for PPP a second time, only one organization stated they would seek additional PPP assistance. Several others stated it would not be necessary, or that they would not be eligible. Most organizations did not experience the 25% reduction in revenue that is required in order to receive a second round of PPP funds.

Initial guidance (or lack thereof) for PPP drawdown and loan forgiveness worried many providers. Leaders had significant concerns about paying back their loan if it were not forgiven. Over time, as the federal government provided more specific guidance to lenders, this uncertainty disappeared. To our knowledge, all providers who received a PPP loan had it forgiven. This success is also attributable to the strong working relationships providers had with their community banks, who offered resources and expertise.

Financial Concerns

Though concern about reducing staffing and meeting immediate needs is better, the uncertainty of future funding remains high.

Over the course of the past year, concerns about organizational financial position have improved but there remain concerns about the unpredictability of the economy and its impact on giving over the coming years. Notably, extreme levels of concern about loss of income, being able to meet expenses, staff reduction, and uncertainty about future funding at the onset of the pandemic has eased significantly, though most respondents still expressed elevated levels of concern about their organizations future financial position.

Of note: 59% of organizations did not have to make any budget cuts and 71% did not have to reduce staff over the past year. Though these figures are remarkable given the broader scope of the pandemic, 41% of organizations were forced to make budget cuts and 29% reduced staff (mostly likely temporarily) over the past year. This is significant given the critical role that many of the respondents have in providing shelter and housing and related services to low-income residents in our community.

FIGURE NUMBER 4.9

Level of concern about loss of income

When asked at the outset of the pandemic about concern over the potential loss of income, 47% of respondents were extremely concerned compared to just 6% at the time of the second survey. However, the majority of respondents (35% somewhat concerned; 18% moderate concern) still expressed above average concern about the continued potential loss of income.

Concerns about meeting necessary expenses remain high, but lower than during the early days of the pandemic. 41% of respondents were extremely concerned about meeting necessary operational expenses, compared to just 6% during the second survey. 18% of respondents indicated no concern at all about expenses though 18% and 29% of respondents expressed Some and Moderate levels of concern respectively.

Concerns about staff layoffs/furloughs showed the largest change between the two survey periods; 18% of respondents expressed no concern about laying off staff at the beginning of the pandemic compared to 47% that felt the same a year later. Significantly, the 35% that expressed extreme concern about staff reductions fell to just 6%. Overall, 71% of respondents indicated that they had not reduced staffing at all over the past year.

FIGURE NUMBER 4.10

Level of concern about uncertainty of future funding

Uncertainty about future funding remains high, and is the category that exhibits the least improvement between the two survey periods. Collectively, 70% of organizations were moderately to extremely concerned about future funding at the inset of the pandemic compared to 59% a year later.

The impacts of the past year are projected to last for years. In order to meet the uncertainties of the coming years, organizations will need to expand services/programming/staffing, improve upon virtual service delivery, normalize health and safety protocols, and incorporate the cost of PPE into their operating expenses.

Philanthropy must continue providing critical support to housing organizations.

We asked respondents a series of questions about resources needed to continue to mitigate the impact of pandemic. 69% of respondents indicated that new funding resources will be very important to meet the continued needs of the pandemic. 38% and 31% of respondents indicated that lifting restrictions or easing requirements on existing funding is important or very important to meeting organizational needs. Majorities of respondents indicated that PPE and other health related measures, additional investments in virtual technologies, and hazard pay or other financial incentives for staff were important or very important to continuing to address pandemic impacts.

When asked about the most important sources of funding during the pandemic, 71% and 24% of respondents indicated that philanthropic support was important or very important. 59% and 24% of respondents said the same about PPP loans, while 47% indicated that local government support was very important.

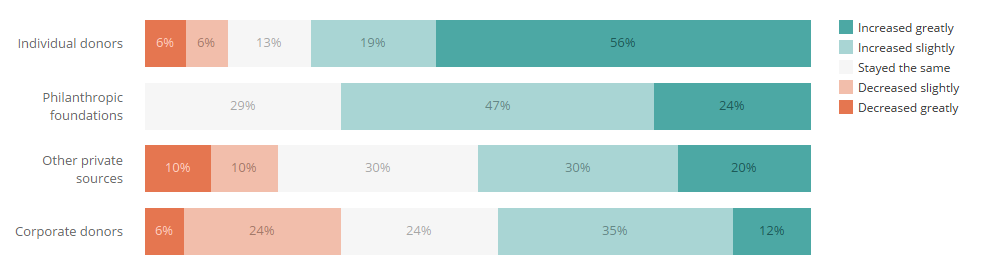

FIGURE NUMBER 4.11

Changes in private funding support

Asked about changes to private funding, 56% of respondents stated that individual giving had increased significantly; 24% indicated that foundation support had increased significantly (30% slight increase); and 12% indicated that corporate funding had increased significantly — 30% of respondents indicated that corporate funding had decreased over the past year.

Client and Organizational Health

Organizations have been largely successful in protecting staff and clients from the physical impacts of COVID-19 but are challenged to address their mental and emotional health needs.

The past year highlighted the intersection of housing and health like no other event in recent memory. No one was spared the impact of the pandemic and organizations providing direct client services were particularly stressed. Similar to the first survey, we asked specific questions about the physical, mental, and emotional health of staff and clients.

Although nearly every provider still expresses at least slight concern about exposure today, the share of respondents who are “extremely concerned” has decreased from 76% to 29%. Most organizations have much less anxiety about exposure thanks to new protocols, reliable sources of PPE, and expanded vaccination activity.

FIGURE NUMBER 4.12

Level of concern about COVID-19 exposure

In regard to the transmission of COVID-19 among staff, only three organizations did not have staff contract the virus; 14 organizations stated that at least one staff member contracted the virus. There was significant discussion around the adoption and implementation of health and safety protocols including standardized procedures for testing, quarantining and symptoms tracking. These procedures differed in response to direct interaction with clients; those directly engaged in resident services obviously adhered to more stringent protocols for residents.

This collective response helped to prevent significant outbreaks and maintain the overall physical health of both clients and staff. In fact, the transmission rate for those experiencing homelessness in the region was lower than the state average. However, the mental and emotional health of staff and clients as they continue to bear the accumulated stress and fatigue of the ongoing crisis is of significant concern.

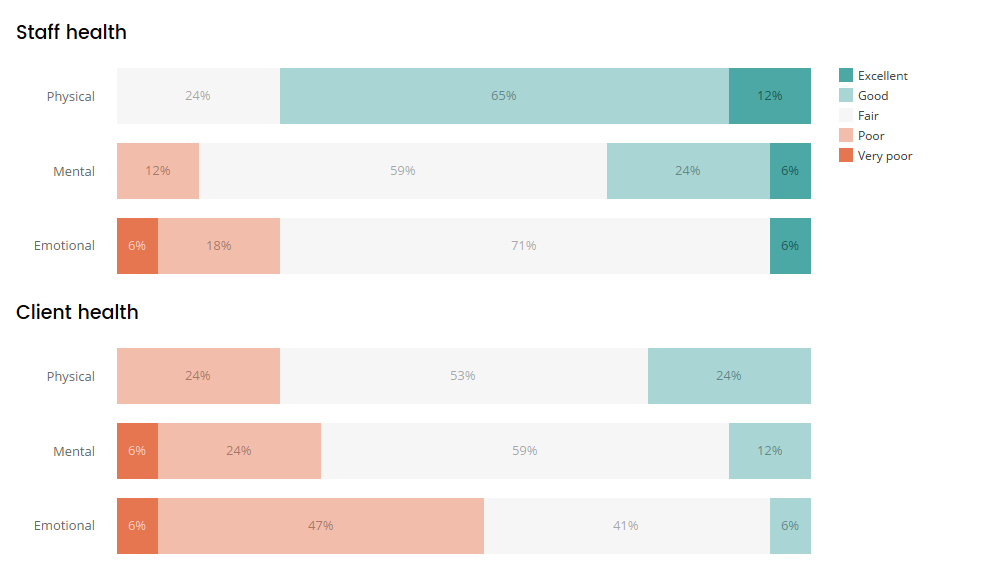

FIGURE NUMBER 4.13

Current physical, mental, and emotional health of staff and clients

Overall, respondents indicated relatively poor physical, mental, and emotional health for both staff and clients. Client health across all three categories was significantly lower than for staff.

Respondents indicated that the physical health of staff was generally good: 24% Fair; 65% Good, 12% Excellent. The majority of respondents (59%) indicated that the mental health of staff was Fair, 24% Good, and 6% excellent. Emotional health for staff suggests cause for concern as just 6% of respondents indicated staff emotional health being Good, 71% Fair, 18% Poor and 6% Very Poor.

Similar to the responses for staff physical health, physical health for clients was seen as being generally fair to good (53% and 24%). Mental health was lower with 59% of respondents indicating that client mental health was Fair, 24% Poor and, 6% Very Poor. 47% of respondents indicated that client emotional health was Poor and 41% Fair.

During follow-up interviews, mental and emotional health was a topic of frequent discussion and concern. Several organizations made inroads into prioritizing the emotional and mental health of staff and clients, through implementing mindfulness training, communicating about existing employee benefit programs and counseling and even having mental health professionals attend staff calls. However, more comprehensive, longer term, and sustainable solutions are needed. The vaccine has provided some hope for a return to some normalcy, eased anxiety of contact in the workplace and has been relatively widely accepted. Though we did not attempt to explore differences in variations between staff and client vaccinations rates, we heard anecdotally that staff acceptance rates were quite a bit higher than for clients even in light of relatively intensive vaccination education. One shelter provider indicated that no residents were receptive to receiving the vaccine.

The pandemic has underscored the relationship between housing and health in unforeseen ways. Long-term connections to resources, both financial and human, to help ensure the mental and emotional health of our non-profit housing providers, clients, and overall infrastructure will be needed in the coming years.