THE FWD #243• 674 words

How the Latest Ruling Deepens America’s Housing Crisis

The Verdict That Changed Everything

In July, a Texas federal judge dealt a crushing blow to 100 million Americans carrying medical debt. By overturning the CFPB rule that would have removed medical bills from credit reports, Judge Sean Jordan essentially ruled that getting sick can permanently damage your housing prospects. The overturned rule would have removed an estimated $49 billion in medical bills from 15 million Americans’ credit reports, potentially approving 22,000 additional mortgages annually and raising credit scores by an average of 20 points.

The Housing Domino Effect

- For Renters: Landlords routinely run credit checks when assessing applications for new rental units, and medical debt can tank your score by 100+ points. Even a $500 medical bill from years ago could disqualify you from an apartment, forcing you into substandard housing or homelessness.

- For Homebuyers: Mortgage lenders are already tightening standards. With medical debt remaining visible, first-time buyers—especially those with chronic conditions—face an impossible catch-22: get treatment and lose homeownership dreams, or skip care and risk catastrophic health outcomes.

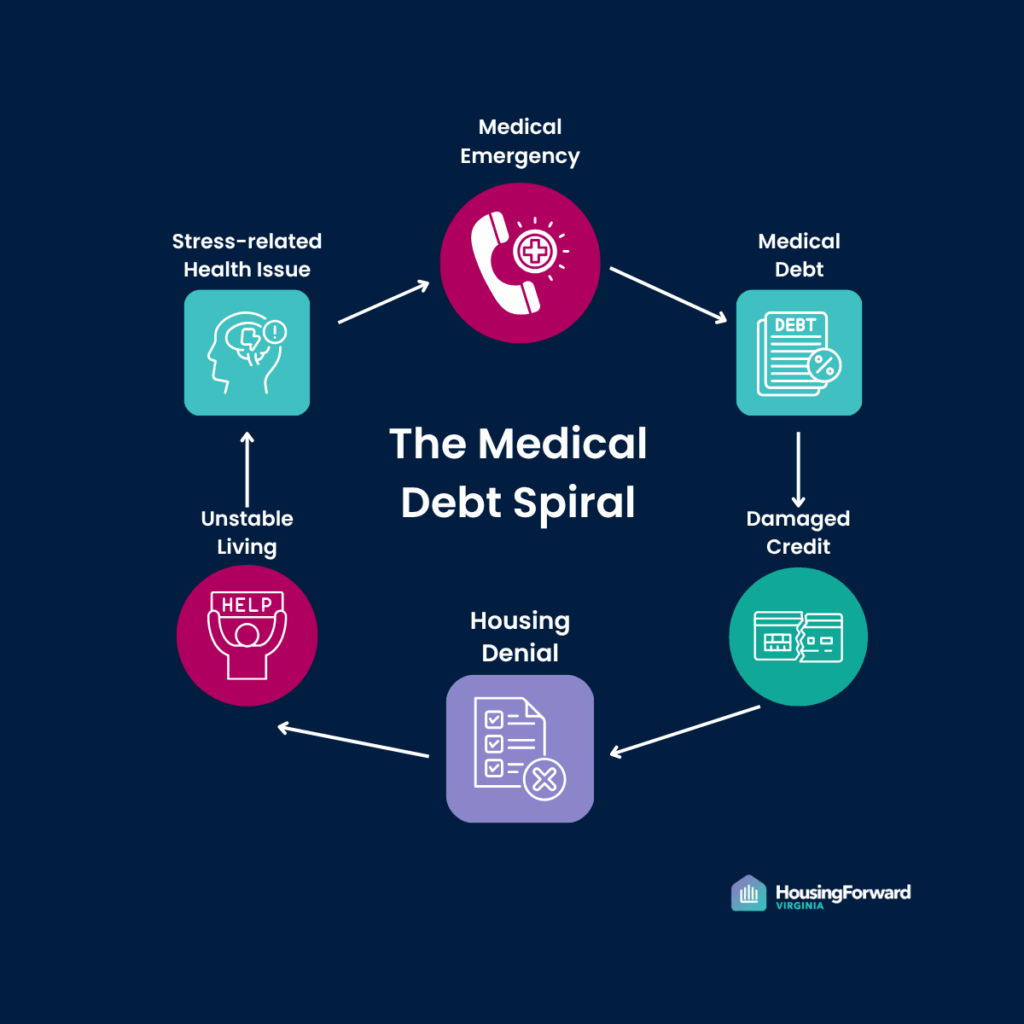

The Debt Spiral Accelerates

This ruling creates a vicious cycle:

Unlike other debts, medical bills often result from emergencies beyond personal control. The CFPB’s own research showed medical debt poorly predicts loan default, yet it continues weighing down credit scores. Additionally, uninsured, black, and hispanic residents are those most likely to have medical debt, furthering the already existing racial equity gap in housing.

Populations uniquely affected by this new ruling include:

- Young Adults: Starting careers while managing student loans now face additional medical debt barriers to their first homes.

- Chronic Condition Patients: Those with diabetes, cancer survivors, and others requiring ongoing care become permanently locked out of quality housing.

- Families: Parents who chose medical care for their children may sacrifice homeownership for their family’s health.

Congressional Context: Policy in Limbo

Congress has been actively examining medical debt policy, with the Congressional Research Service tracking multiple legislative proposals including H.R. 1773, H.R. 6003, and S. 2483. However, Congressional Republicans have consistently opposed the CFPB’s efforts to remove medical debt from credit reports, creating a partisan divide on healthcare-related financial protection.

The CRS notes that medical debt presents unique policy challenges because it often stems from emergencies beyond consumer control, yet significantly impacts creditworthiness. This ruling essentially freezes progress on comprehensive medical debt reform at the federal level.

What This Means Right Now

- Credit Scores: Medical collections will continue dragging down scores for 7 years, with newer debts having maximum impact.

- Housing Applications: Expect more rejections, higher deposits, and requirements for co-signers.

- Market Segmentation: A two-tiered housing market emerges—those with clean medical histories versus those trapped in medical debt.

Finding Light in Dark Times

While federal protection is gone, solutions exist at multiple levels:

- State-Level Action: Thirteen states already limit medical debt’s credit impact, with more considering legislation

- Congressional Activity: Multiple bills remain in play, including ongoing efforts to revive federal protections through new legislative approaches

- Credit Repair: Dispute inaccurate medical collections and negotiate payment plans—the CFPB’s 2014 research showed medical debt is a poor predictor of loan repayment

- Alternative Lending: Seek lenders who use alternative credit models beyond traditional reporting

- Nonprofit Support: Organizations like RIP Medical Debt are buying and forgiving medical collections

For comprehensive policy analysis, Congress members and staff can reference the Congressional Research Service overview (IF12169) updated through August 2025.

The Bottom Line

This ruling doesn’t just affect sick people—it impacts anyone who might get sick, which is everyone. By treating medical debt like credit card debt, we’re essentially saying healthcare is a luxury that should determine where you can live.

The housing crisis just got deeper, and it’s going to take coordinated state-level action, lending innovation, and advocacy to dig out. Because in America, getting well shouldn’t mean you can’t get housed.