FWD #261 • 475 words

New data shows mortgage defaults rising fastest among borrowers under 30 — but we’re nowhere near 2008.

Each quarter, the Federal Reserve Bank of New York releases its Household Debt and Credit report, drawing on a nationally representative sample of Equifax credit data covering roughly 44 million individuals. It tracks balances, originations, and delinquency rates across every major debt type — mortgages, auto loans, credit cards, student loans, and home equity lines. For housing practitioners, it’s one of the most reliable early-warning systems available.

The latest release, covering Q1 2026, shows household debt essentially flat at $18.8 trillion — up just $18 billion from the prior quarter. Mortgages account for 70% of that total. Even small shifts in delinquency or foreclosure rates move large numbers.

Not Looking Great for Young Homeowners

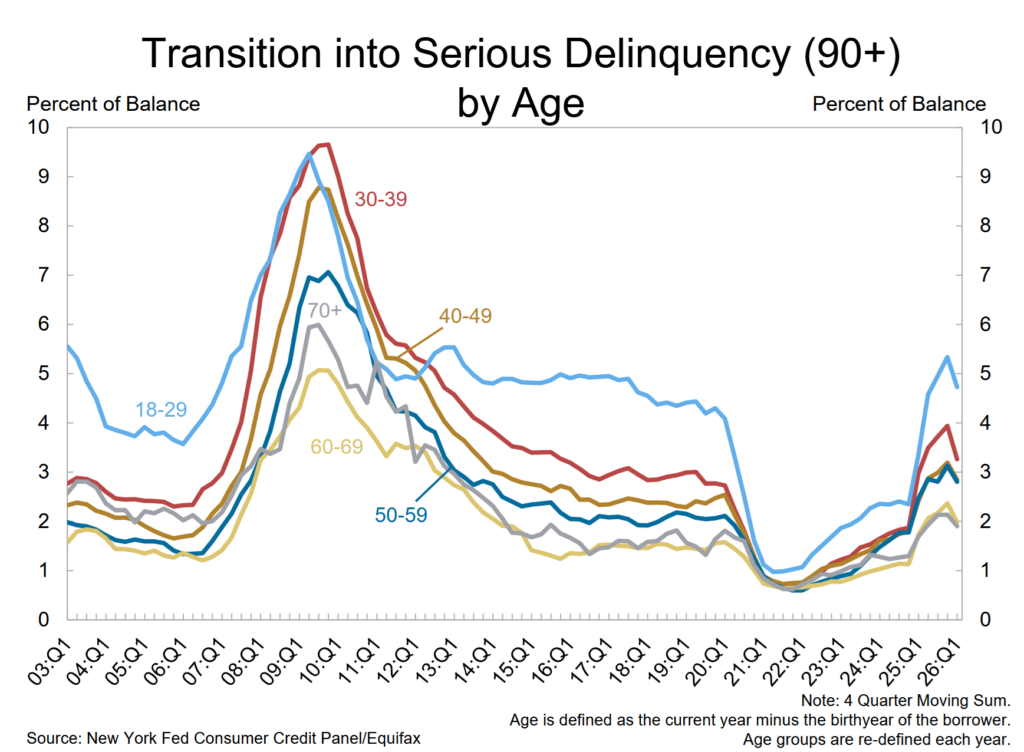

One chart in the report merits particular attention. The “Transition into Serious Delinquency by Age” chart tracks the share of mortgages 90 or more days past due, broken down by borrower age. The 18–29 cohort is the light blue line stretching well above the rest as of 2025.

The dominant story is the massive spike around 2009–2010, when the 30–39 age group hit nearly 9.5% — a generation of young homeowners who bought near the peak getting crushed.

After a decade-long decline and a pandemic-era lull, when forbearance programs effectively suppressed delinquencies, all age groups bottomed out around 2021–2022 at historic lows near 1%.

Now, every cohort is climbing again. The 18–29 group is rising fastest and most sharply. By the end of 2025, over 5% were seriously past due on their mortgages.

Student loan delinquencies among young borrowers compound the pressure. The report shows student loan balances 90 or more days past due running at 10.3% nationally — up from 9.6% last quarter, and still elevated from the resumption of payment reporting after pandemic forbearance ended.

Broader Stress Across the Market

The stress isn’t isolated to young borrowers. As of March, 4.8% of all outstanding debt was in some stage of delinquency — flat from Q4 2025, which offers modest reassurance.

Early mortgage delinquency actually ticked down slightly, from 3.9% to 3.8%. But the share of mortgage balances transitioning into serious delinquency (90+ days) edged up from 1.4% to 1.5%, and about 59,000 individuals had new foreclosure notations on their credit reports — a slight increase from the prior quarter. Third-party collections worsened too, with 5.0% of consumers carrying a collection account.

HELOC balances rose for the 16th consecutive quarter, now totaling $446 billion — $129 billion above the post-pandemic low. Homeowners are drawing on equity at a steady clip, which could amplify stress if home values soften.

What to Look Out For

The 30–39 cohort, now carrying large mortgage balances taken on during the 2020–2022 buying frenzy, is the one to watch. The chart shows they led the crisis last time, and they’re rising again.

Delinquency rates remain well below 2008–2010 peaks. But the trajectory heading into the rest of 2026 warrants our close attention.