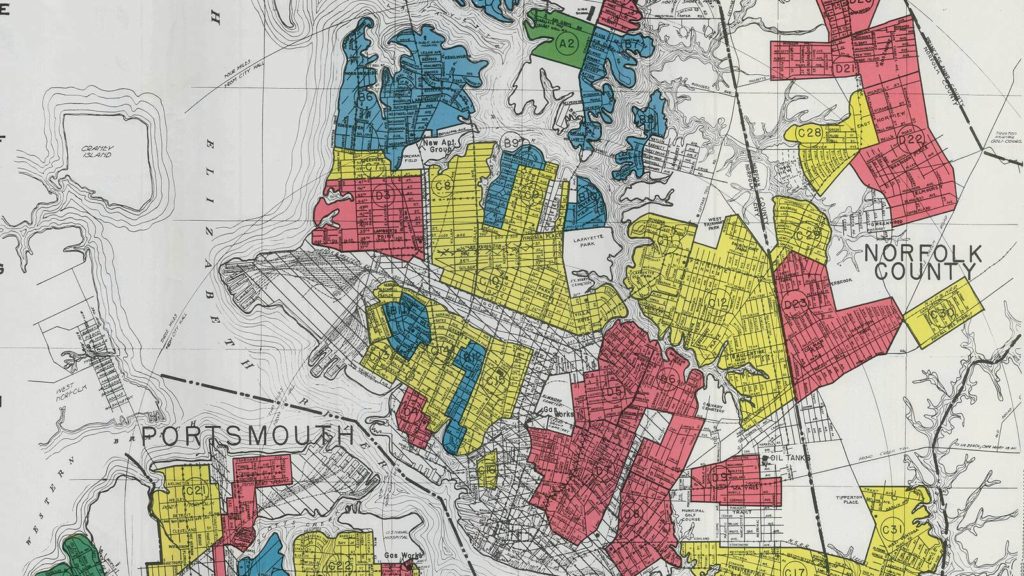

Image: The 1940 Home Owner’s Loan Corporation map of residential lending risk in Norfolk, showing the “highest risk” Black and low-income neighborhoods in red.

The FWD #B07 • 652 Words

We’ve pushed banks to invest in communities of color for forty years. What else will it take to make a difference?

The Community Reinvestment Act has long been a focus of regulatory attention. It’s undergone plenty of changes since its inception. So what is this law all about, and why are we paying attention to it today?

What is the Community Reinvestment Act?

The Community Reinvestment Act (CRA) is a community development law that intends to ensure access to credit for all communities. For banks to receive federal deposit insurance (FDIC) to protect their accounts, they must comply with the CRA by lending, investing, or providing services in communities where they have branches (and take deposits) or where the bank lends.

Banks will receive credit and grades from federal regulators (including the Federal Reserve) for CRA activities focused on improving the financial health of low- to moderate-income households and neighborhoods.

President Jimmy Carter signed the CRA into law in 1977. The bill’s primary author in congress, Senator William Proxmire of Wisconsin, sought to tap into the financial power of banks and financial institutions to change communities—as opposed to relying on government programs and funding to revitalize American cities.

Why was it needed in the first place?

Even into the 1970s, banks were reluctant to lend in urban centers and to communities of color, since better returns could be found in whiter, more affluent areas. This practice follows a well-documented history of predatory banking and lending practices, including redlining.

The CRA was the first major attempt to ensure that Black and Brown communities, continually denied access to credit and lending in the past, would now see the investments that their communities and households needed. In some ways, the CRA was an epilogue to major civil rights legislation from the 1960s.

What has the CRA accomplished?

Since its adoption, the CRA has provided opportunities for communities of color to access credit and investments. But have these opportunities materialized into meaningful progress?

The short answer is that it’s complicated. Measuring the impact of a multifaceted, multi-sector, nationwide regulatory framework at the neighborhood level is difficult. Sometimes, the same report can suggest marked improvements in lending and vacancy in CRA-designated census tracts, right alongside evidence that points to no effect at all.

How do CRA regulations change?

Advocates and regulators have long proposed CRA reform to modernize the law in search of steeper gains in Black homeownership and wealth generation for communities of color, which have remained stagnant in recent years.

The Black homeownership rate in Virginia has remained at or below 51 percent over the CRA’s lifespan.

This desire is not new. Now more than 40 years old, policymakers have changed the CRA on a regular basis, often in response to major shifts in market conditions. Today, the CRA must now account for a modern society with tools unimaginable in the 1970s—like internet banking!

Federal bank regulatory agencies are currently accepting public comment on their proposed changes to the CRA, which include:

- “Expanding access to credit, investment, and basic banking services in low- and moderate-income communities;

- Adapting to changes in the banking industry, including internet and mobile banking;

- Providing greater clarity, consistency, and transparency;

- Tailoring CRA evaluations and data collection to bank size and type;

- Maintaining a unified approach.”

So far, these draft reforms have been met with mixed reviews from the housing sector. While some were initially supportive, many advocates would now like to see a greater commitment to race-conscious lending, which we covered back in March.

In the current environment, most banks already receive “satisfactory” or “outstanding” CRA ratings. Without new specific and intentional commitments to racial equity, advocates fear that patterns of disinvestment could continue without consequence.

How can I share my opinion with regulators?

You can read the proposal and make a public comment on the proposed changes to the CRA here. Submissions are due by next Friday, August 5, 2022.

What programs, policies, and issues do you find most challenging to explain to policymakers? Let us know, and your suggestions may show up in a future edition of Back to Basics.